Third Sector organisations in Leeds continue to face financial challenges, affecting staff, services and, to a lesser extent, organisation viability.

The results capture the experience of a cross section of third sector organisations in Leeds. This is the first time we have asked about which risk factors are of highest concern, and whether organisations are in a better or worse financial position compared to last year.

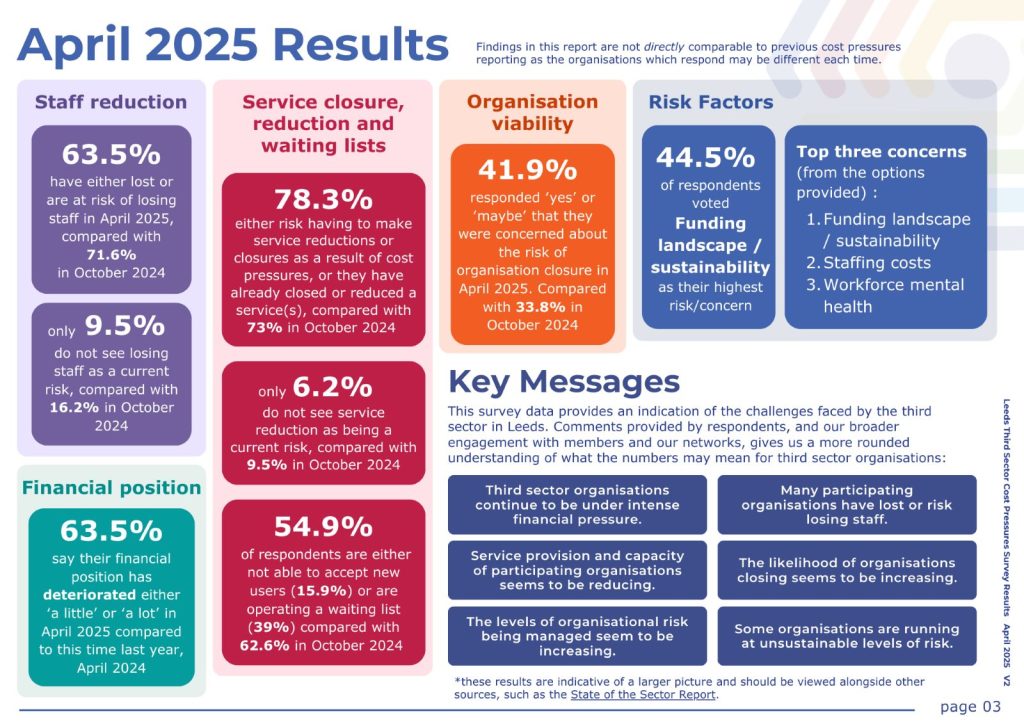

The top three organisational risks from the options were:

- Funding landscape / sustainability.

- Staffing costs.

- Workforce mental health.

As well as significant organisational risk, the results also show evidence of the sector’s resilience, proactive approach and dedication to the people they serve.

A strong, supported, well resourced and embedded third sector is needed if we are to shift our health and care system in line with national and local ambitions. Delivering on the Neighbourhood Health agenda through partnership working and collaboration.

Read the report:

- April 2025 Cost Pressures Survey Results (google doc) – This document has a detailed breakdown of each questions responses with charts. From p.13 there is a large selection of comments from respondents, anonymised and grouped into themes which provide rich examples directly from organisations.

- April 2025 Cost Pressures Survey Results and Summary of results to date (presentation link)

April 2025 Cost Pressures Survey Results and Summary of results to date (pdf for print)

This is a shorter presentation and formatted pdf. It contains the same key data points as in the document. It then goes on to collate data from ALL the surveys to date into tables and stacked bar charts. - All previous survey results and the 2022 – 24 summary are available on our Forum Central Cost-of-Living and Cost Pressures page.

Headlines

This survey ran between 6 March and 7 April 2025. A total of 74 organisations responded.

Comments provided by respondents, and our broader engagement with members and our networks, gives us a more rounded understanding of what the numbers may mean for third sector organisations:

- Third sector organisations continue to be under intense financial pressure.

- Many participating organisations have lost or risk losing staff.

- Service provision and capacity of participating organisations seems to be reducing.

- The data indicates that the likelihood of organisations closing seems to be increasing.

- The results indicate that the levels of organisational risk being managed are increasing.

- Some organisations are running at unsustainable levels of risk.

Please note these results are indicative of a larger picture and should be viewed alongside other sources, such as the State of the Sector Report. Findings in this report are not directly comparable to previous cost pressures reporting as the organisations which respond may be different each time.

Excerpt of Data

- Workforce:

- 63.5% of respondents said that they have either already lost staff (28.4%) or they are at risk of losing staff (35.1%) as a result of cost pressures.

- Only 9.5% of respondents (7 organisations out of 74) did not think that their organisation risked losing staff. (Compared with 16.2% last October).

- Services:

- 78.3% of responses indicate that they had either closed services (13.4%) and/or reduced services (21.6%), and/or that they risk having to make service reductions or closures (43.3%) as a result of cost pressures.

- Only 6.2% (6 organisations) did not see service reduction as being a risk.

- Closure:

- 41.9% of respondents answered ‘yes’ (13.5%) or ‘maybe’ (28.4%) to organisation closure being a current risk. (Compared with 33.8% last October).

- Financial Position:

- 63.5% of respondents reported that the financial position of the organisation has deteriorated a little (31.1%) or a lot (32.4%), compared to the same time last year.

Quotes

“Grant income has significantly reduced with funders narrowing criteria or closing for new applications.”

“A more collaborative approach would be very helpful but I think there is pressure to compete.”

“It is a very tough climate to be working in and the prospects do not look promising.”

“We believe partnership working is key but feel there are less opportunities than there have been in previous years to do this.”

“We have cut back on growth to enable us to prioritise quality of service.”

How partners can support and strengthen the sector

As ‘funding landscape / sustainability’ came out as the highest concern to third sector organisations which responded, there is an opportunity for commissioners and funders to explore ways the sector can be strengthened through better approaches to funding and commissioning.

Commissioning is one of eight ambition strands set out in the Leeds Third Sector Strategy – highlighting the need for partners to ‘invest in who is best placed to design and deliver services’ and for commissioning to be ‘based on trust, values and flexibility.’ This strand is a priority areas of focus for TSL (Third Sector Leeds). Further detail can be found on page 16 of the Third Sector Strategy.

Partners can also uphold the Leeds Commissioning Code of Practice approved by Leeds Third Sector Partnership in 2018 which remains just as relevant today. It covers in detail how commissioning should happen in Leeds, including principle around:

- full cost recovery

- giving 6 months notice for funding changes

- for decommissioning to be based on needs and equality impact assessment.